Yeah that's my first reaction to. 1.2% doesn't sound much. It's just people making headlines out of thin air. If it lists the water and energy consumption I might be more concerned.

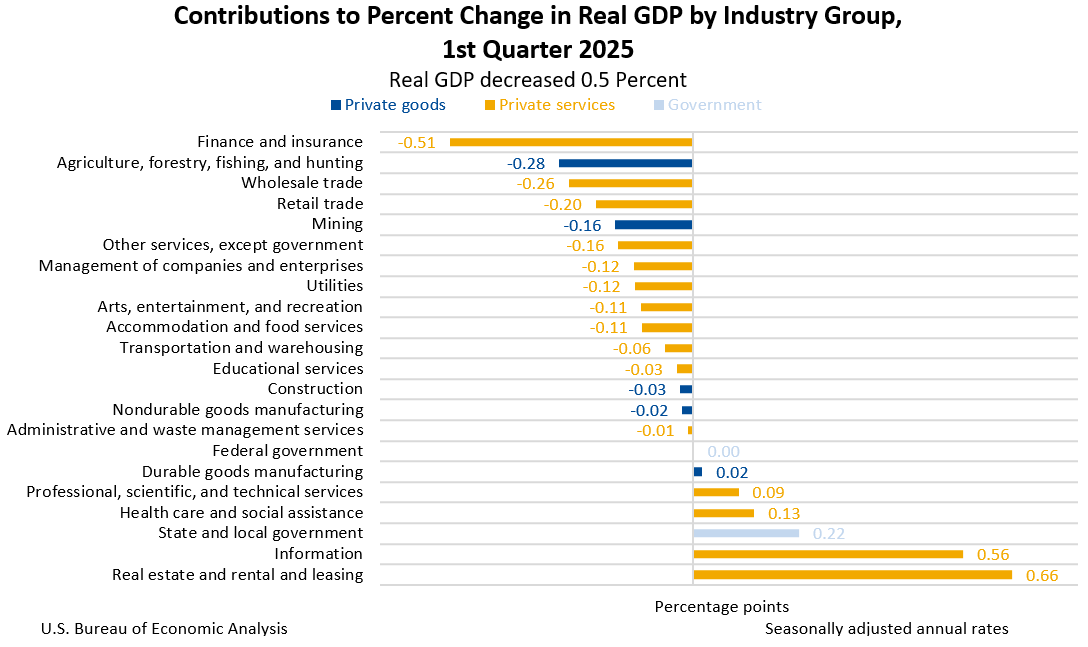

Slightly off-topic, but ~9% of GDP is generated by "financial services" in the US. Personally I think it's a more alarming data point.

I have read, but not verified the figures myself that if the United States had Australia's healthcare system - universal, government funded healthcare (excluding dental) then all US citizens would have near free healthcare, would not need costly insurance, and the government would spend a similar amount to what it does now

According to O3 US public health spending (state + federal) is 8.6% of gdp. For perspective, here's a list of countries with universal systems which spend less (these numbers include private spending), and life expectancy (US is 78.4 for reference):

So it seems like we could have universal coverage and higher life expectancy if the US government simply spent exactly what it is currently spending, but on everyone, rather than just the old, poor, and veterans.

There is a factor for the US effectively subsidizing these countries by having our current system. Healthcare companies make their bread in the US and get scraps elsewhere in the world.

This drives an enormous amount of innovation, and the near complete dominance of US healthcare companies in the west reflects that.

The US moving to a universal healthcare model would likely kill the lucrative US market, and while providing cheaper healthcare, it likely wouldn't make them dramatically cheaper while also having the effect of driving up costs in other western countries.

A bit like a balloon, where the profits are swelled in the US and limp elsewhere, squeezing the US will ha global effects.

Anyone that lives in a country with universal healthcare only knows it's a no-brainer because they have the American nightmare of a health care system to compare it to. Seriously, I don't know how/why Americans put up with the stress of one serious medical event potentially financially ruining your life.

Ultimately, "financial services" is what's downstream of insurance, banking (deposits / money transfers), loans and retirement savings. Also efficient capital allocation and the provision of government services to some extend. Those are things we want, and we want those things to work well.

Why is 9% for financial services bad? This should cover fees/interest from everything like loans, transactions, mortgages, advice, investing, etc. It doesn't seem that surprising to me that the systems that are the backbone for all the money operations that power the rest of the economy make up about 10%.

I get your point, but the flip side is that private companies like visa and Mastercard get to skip 2.5%+ off the entire economy. Visa has more than 50% profit margin, and it’s not like these companies are innovating with all that extra cash either. It’s just money from my pocket to some rich investor somewhere

Visa and Mastercard aren’t skimming 2.5% off the economy; the majority of the interchange fees go to banks (which Visa is not; their actual product is VisaNet which provides payment infrastructure, broadly.)

Trivially verifiable by Visa’s revenue being $35B, which is not even close to 1% of just US GDP (about $30T).

Cash costs more nearly that much when you count all the time spent counting and recounting it - at least 8 times for every transaction. (the buyer finds and counts, then the cashier counts, then count change. Then the manager counts and recounts the till, finally the bank counts and recounts it - several of the above will come up with a miscount and recount additional times to verify). Then we add crime loss on top of that.

Or your retirement account. Everyone is mad about investors and companies making money. Sure, there are ultra wealthy people (mostly founders) that benefit disproportionately. However, most people who hope to retire some day rely on a 401k, pension, etc which is dependent on stocks. Retirement accounts have about $36T in the US, mostly in equities and corporate bonds.

"Founders" are a tiny percentage of the rich, they're just the ones in the news.

The richest 1% own half the wealth in the world and the gap is getting wider. Since 2020, for every dollar of new global wealth gained by someone in the bottom 90%, one of the world’s billionaires has gained $1.7 million. (Source: https://www.globalcitizen.org/en/content/wealth-inequality-o...)

So yes, some of the wealth is going to your retirement account. But for every penny going to a middle-class professional workers retirement, there's about a thousand dollars going to some hedge fund manager or the trust fund of the grandson of some robber baron who got rich a hundred years ago.

Interests you pay is not necessarily all financial services revenue. Only the net interests the industry receives count as revenue. There's a lot of netting going on in finance.

"Inefficient" implies the money is being burned or something. It's flowing into the pockets of people who work in the financial services industry, who then spend it on other things. The economy isn't zero-sum.

And the industry itself greases the wheels of other industries. In other words without financial services like lending and payment processing there would be less spending and investment overall, so other industries would shrink along with it.

You’re falling for the broken window fallacy, it’s inefficient as demonstrated by automation reducing the percentage of the economy devoted to financial services without any negative effects.

Banking used to really suck. Walk into an old bank building and it looks empty with spaces for a dozen tellers never actually used, this is a good thing as nobody actually wants to stand in line at a bank. People have largely stopped using cash because swiping a card is just more pleasant.

Meanwhile payment networks (Visa, Mastercard) have over a 50% profit margin, that’s a huge loss for the US economy. Financial services dropping to 1% of the overall economy would represent a vast improvement over the current system.

Retail Banking =/= Finance. You cannot easily standardize let alone automate a corporate merger or raise capital from various sources due to unique individual characteristics of each company, that's why investment banks exist.

The Retail Bank's main function isn't providing cash either, it's keeping deposits which they loan out for profits. Whether you use cards or cash won't affect those margins.

While LLM’s are nowhere near this capacity today, it’s likely future AI systems will be able to handle such complexities just fine. Competition + automation means the financial sector really is on a long term decline. Some things aren’t automated due to customer preference, but preferences change over time.

> The Retail Bank's main function isn't providing cash either, it's keeping deposits which they loan out for profits. Whether you use cards or cash won't affect those margins.

The margins on loans have decreased significantly as shown by much lower effective interest rates relative to inflation.

The effort associated with loans have been reduced significantly as credit checks, automated repayment, etc have reduced the risks and overhead. Competition between banks means their profits are a function of costs, thus driving down costs has reduced in the overhead on loans.

Is there any evidence that central planning on a much larger scale is drastically more efficient? We're talking about a whole country, after all. I take your point that companies themselves are usually centrally planned internally, but centrally planned economies haven't fared so well.

> Is there any evidence that central planning on a much larger scale is drastically more efficient?

If it were, why do we have more than one company?

> I take your point that companies themselves are usually centrally planned internally

Well, sort of. It is true that companies exist solely for the reason of exploiting efficiencies in central planning. If central planning was always inefficient, companies wouldn't exist! But, as I alluded to earlier, no company has found central planning to be efficient in all cases. Not even the largest company in the world centrally plans everything. Not even close.

As with most things in life, a bit of balance will serve you well.

Large companies are all decentralized. The ceo will set broad direction but they always leave details to the lower levels. Those lower levels often do things that are against the needs of a different division. Companies are reorganizing for efficiency all the time.

> Large companies are all decentralized. The ceo will set broad direction but they always leave details to the lower levels.

Typically, central planning does not imply micromanagement. The "broad direction" you speak of is the central planning.

> Companies are reorganizing for efficiency all the time.

But, of course, companies wouldn't exist if markets were perfectly efficient. The sole reason for companies is to exploit the efficiencies of central planning. But, of course, just as if markets were perfectly efficient there would be no companies, if central planning was perfectly efficient there would only be one company, so... Like always, there are tradeoffs that we have to find balance in.

I can't help but wonder if there's a middle ground between people not being able to obtain credit to pursue new enterprises, and entire productive enterprises being swallowed up in the pursuit of short-term rent seeking.

Could such a middle ground exist? Sure. Could someone design a system where that middle ground was a natural equilibrium? Unsure. I don't see how you incentivise the goldilocks behaviour (but I am not the smartest bear so maybe someone else can)

There's a good book on this topic by a Scottish philosopher: An Inquiry into the Nature and Cauſes of the Wealth of Nations by Adam Smith, LL. D. and F. R. S, formerly Profeſſor of Moral Philoſophy in the Univerſity of Glasgow.

The economy is not a fixed pie that you can just take slices from one sector and give them to another. Financial services provide liquidity that supports every other sector; getting rid of them would cause contraction in every other sector.

That's true to a degree. But giving them free reign inventivizes the kind of behavior that gave us the 2008 financial crisis. So the commenter can be forgiven for wanting to limit that sector.

I'm banking on Space Emperor Elon. If he can form a Musk Sphere around Mars, he should be able to generate enough energy to push Deimos into Earth reasonably fast. Of course, he doesn't have to actually do it. Instead, he could extract tribute and demand we push 50M people into a volcano each year in exchange for not extincting us. In just a few decades, most all our issues resolve.

some years back I was talking to an acquaintance through my daughter's kindergarten and complaining about this point and he said it was because financial services was where all the innovation was happening (he was an investment consultant of some sort)

{kind=link}

Slightly off-topic, but ~9% of GDP is generated by "financial services" in the US. Personally I think it's a more alarming data point.